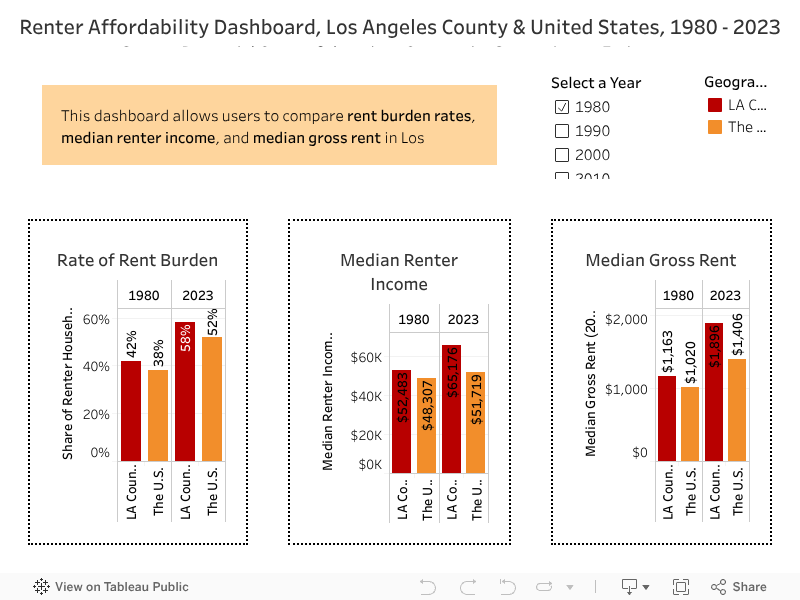

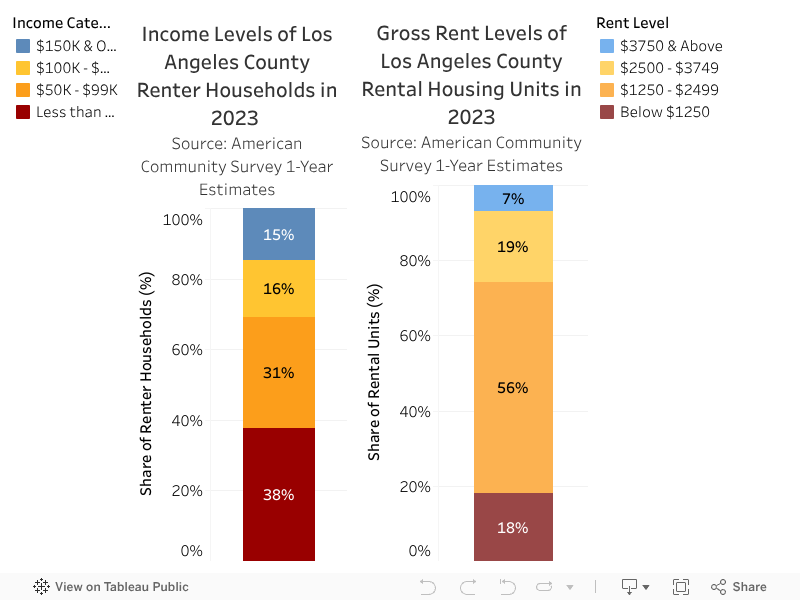

- Median rent throughout this chapter is measured as gross rent, which includes rent price plus the cost of utilities like electricity, water, gas, and sewage.

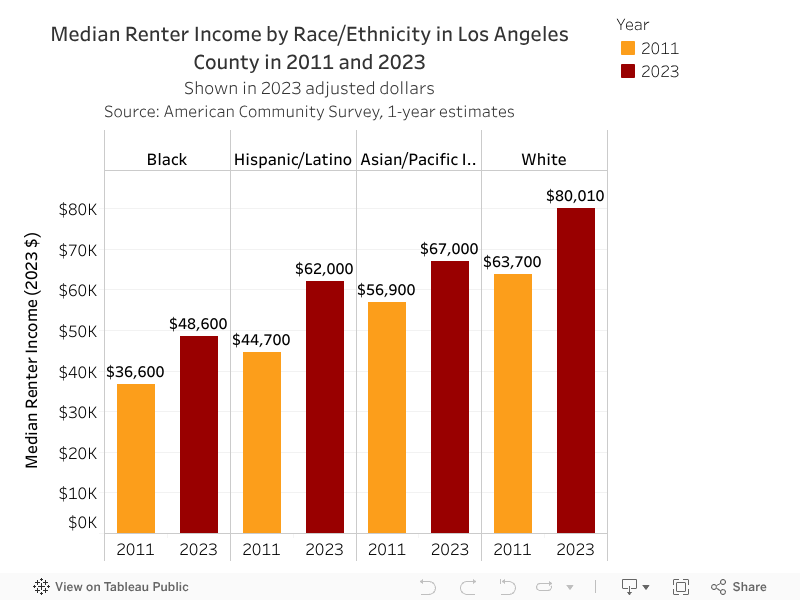

- Household income is calculated by adding the individual income of the head of a household and the incomes of all other inhabitants above 15 years of age, regardless of their relation to the head of the household. Income is defined as any money that a person earns from work, selling products or services, or any other streams such as Social Security payments, pensions, child support, public assistance, annuities, money derived from rental properties, interest and dividends, etc.

- The Great Recession refers to the global economic downturn that began in December 2007 and lasted until June 2009. It was the most severe financial crisis since the Great Depression of the 1930s, triggered by the collapse of the housing bubble and the subsequent banking and financial crisis. The housing market crash, particularly the subprime mortgage crisis, led to widespread foreclosures, massive job losses, and a sharp decline in consumer wealth, severely impacting both the U.S. and global economies.

- “Adjusting for inflation to 2023 dollars” means using an inflation index, such as the Consumer Price Index (CPI), to account for changes in the purchasing power of money over time. This adjustment allows for a more accurate comparison of values from different years by expressing them in terms of the same dollar value.

- In June 2026, we issued a correction for these numbers (previously 59,000 for 2010 and 80,000 for 2023). We updated our methodology to be more exact, and will use this methodology in future reports moving forward. See the SOLACHAN 2026 Data and Methods for a detailed explanation.

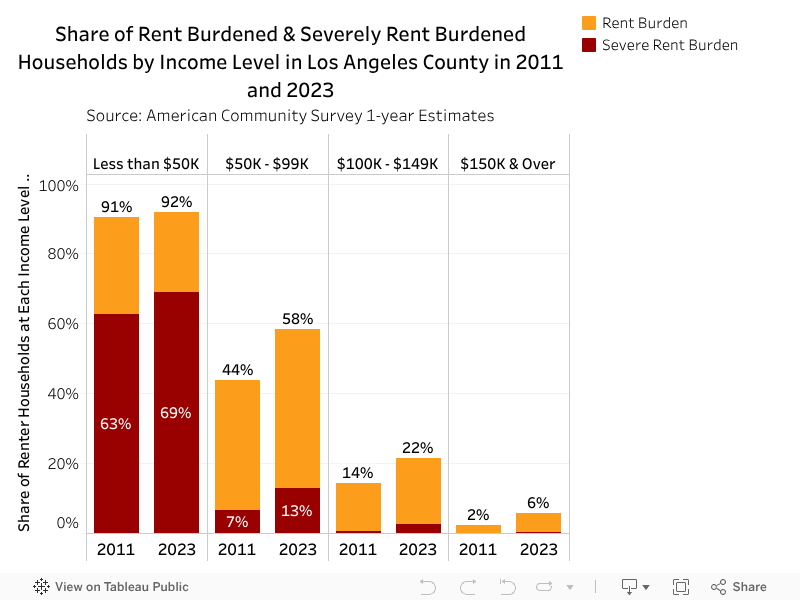

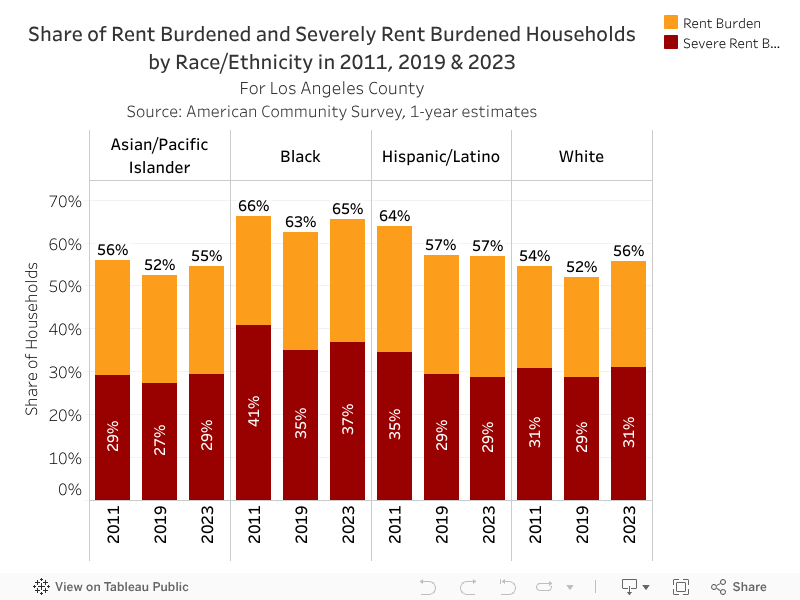

- Rent is considered affordable if a household pays no more than 30% of their income towards rent and utilities.

The race/ethnicity of a household is determined by how the head of household (the person whose name is first on the lease or mortgage) defines their own race/ethnicity. Therefore, this definition of race/ethnicity at the household level may not correctly identify all household members in interracial households

- Income includes other streams outside of wages such as Social Security payments, pensions, child support, public assistance, annuities, money derived from rental properties, interest and dividends, etc

- The “age of a household” is determined by the age of the head of household (the person whose name is first on the lease or mortgage).