Boyle Heights Residents Face Significant Barriers to Homeownership

High rates of homeownership, defined as the percentage of housing units occupied by the owner of the unit, are typically associated with important neighborhood benefits and connections that are a key measure of a stable economy. Additionally, homeownership has long been recognized as a pathway to financial inclusion and economic stability.

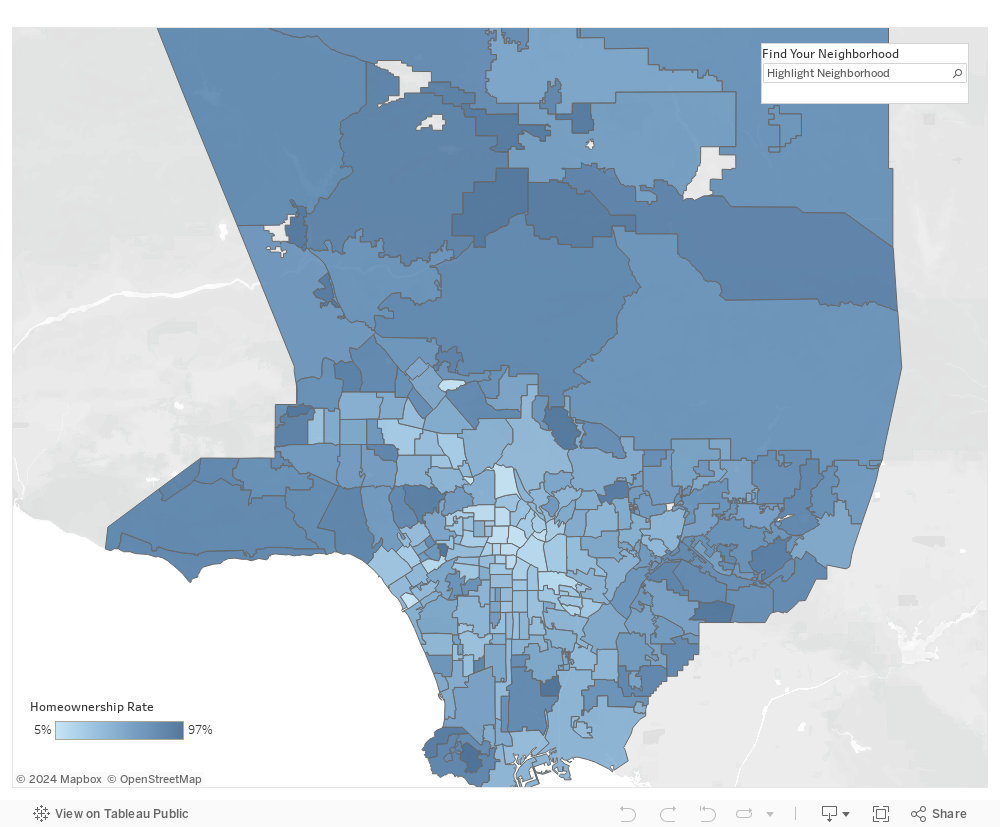

But for many neighborhoods in Los Angeles County, the barriers to homeownership are seemingly insurmountable. Boyle Heights, for example, has consistently reported a homeownership rate of only 23% since 2010. This is significantly lower than neighboring communities of El Sereno, Monterey Park, and East Los Angeles, which have respective homeownership rates of approximately 48%, 53%, and 34%. This data story, developed in partnership with the Leadership for Urban Renewal Network (LURN), explores the challenges and opportunities surrounding homeownership in Boyle Heights.

Barriers to Homeownership: Access to Finance

Access to capital is a significant barrier to homeownership for many residents. The median household income in Boyle Heights is $32,463, significantly less than the median L.A. County household income of $56,196. Higher income can provide the necessary funds to cover monthly expenses such as rent, utilities, groceries, and transportation costs, and have enough leftover to save for a down payment on a home. While income may be one barrier to homeownership, institutional barriers may also prevent higher rates of homeownership.

In addition to access to capital being a significant barrier, poor credit history, or the complete lack of credit history, are additional significant barriers that were identified in a study conducted on property ownership trends in Boyle Heights. LURN surveyed more than 400 Boyle Heights residents to better understand their personal experiences with property ownership in their community. When asked if they have ever applied for a loan to purchase any form of land-based property, 51% responded “No.” Of those that responded “No,” 24% percent identified their credit, or lack of credit, as the central reason.

Access to financial institutions is vital for residents to gain economic stability by having access to basic financial building blocks such as savings accounts and access to credit that can mean the difference between living paycheck-to-paycheck and accumulating the wealth necessary to purchase a home. Boyle Heights has a total of 7 banks to serve more than 91,239 residents. The lack of access to financial institutions may help explain some of the additional findings from LURN’s property ownership study. In addition to surveys, LURN convened a focus group with community residents to gain a deeper understanding of collected survey data. Participants in LURN’s focus group identified several additional challenges to homeownership including a lack of access to reliable personal financial information and a general mistrust in formal, financial institutions as a result of poor information and predatory financial services such as payday lenders.

Even if a resident and would-be home buyer, had the income, savings, adequate access to affordable credit and reliable sources of financial information, rising home values may still put homeownership out of reach. The median home value in Boyle Heights, according to Zillow, has increased from $217,000 in November of 2009, at the height of the great recession, to more than $440,200 as of December 2017. As home values increase, the challenges of affording a home become harder to overcome as buyers would need to qualify for a larger mortgage and save for a more substantial deposit.

Immigration Status and Linguistic Isolation

Many other barriers to homeownership confront residents of Boyle Heights and other communities such as Northeast Los Angeles including immigration status and linguistic isolation.

Nearly one-in-three Boyle Heights residents are non-citizen immigrants. Non-citizen immigrants are individuals that are not United States citizens but may be permanent residents with authorization documents, temporary migrants such as foreign students, humanitarian migrants such as refugees, and migrants without authorization documents.

Homebuyers without social security numbers may apply for a mortgage using an Individual Tax Identification Number (ITIN) provided by the Internal Revenue Service. Immigration status can significantly increase the amount individuals must save and earn to afford a home as ITIN mortgage applicants must have a 20% down-payment and will likely have a higher interest rate than traditional mortgages if the applicant is approved. Many neighborhoods in Northeast Los Angeles also have high percentages of non-citizen immigrants with the highest number in Lincoln Heights (30%) and Cypress Park (25%).

From a national perspective, the Pew Research Center found that nearly 35% of unauthorized immigrant households are homeowners, which is half the rate of native-born households. Unauthorized immigrant households also pay more than $3.6 billion in property taxes each year, according to the Institution on Tax and Economic Policy.

Households with limited English speakers often face unique challenges when navigating the process of purchasing a home including access to bilingual information, applications, and resources. Lincoln Heights (31%), Boyle Heights (29%), and Cypress Park (23%) have the highest rates of linguistic isolation. According to the U.S. Census, linguistic isolation is measured by the percentage of households in which all members of the household that are older than 14 years old have at least some difficulty with English. Linguistic isolation is much more complicated than measuring proficiency in English. For instance, the New York Times found linguistic isolation varied widely among the Spanish speaking immigrant community in New York City where some individuals spoke indigenous languages that few understand, further isolating them from their community.

Solutions and Ideas

Addressing low homeownership rates requires a multi-faceted approach that addresses the various barriers to homeownership such as affordability, access to credit, immigration status and linguistic isolation.

A recent report by Gary Painter, Director of the USC Sol Price Center for Social Innovation, and Stuart Gabriel, Director of the UCLA Ziman Center, identified key policy recommendations that address affordability including easing regulations on residential density and parking requirements as well as inclusionary zoning for affordable housing.

In addition to macro-level policy solutions, LURN’s property ownership study made key recommendations that work directly with residents to help build their capacity toward gaining greater economic agency in their community. A key recommendation made by LURN involves helping community residents better understand their credit histories and how to improve certain personal financial metrics such as income ratios and loan to income ratios that make or break an individual’s ability to access affordable forms of capital. Another recommendation considers highly innovative strategies to better support disenfranchised communities own portions of their neighborhoods including a cooperative, shared ownership concept. A shared ownership concept focuses on granting community residents with direct control over specific properties in their neighborhoods that may help increase a community’s economic agency and wealth.

Boyle Heights and similar communities throughout Los Angeles County remind Los Angeles of its pioneering spirit and the diverse roots that make our communities beautiful and strong. By removing barriers to homeownership, policymakers can help build pathways to opportunity for Boyle Heights residents, and other thriving Los Angeles neighborhoods.

Juan Lopez

Juan Lopez is a first-generation American, a proud product of public schools and the first in his family to graduate college. Juan is currently pursuing a Masters in Public Administration at the University of Southern California Price School of Public Policy. He attended Long Beach City College and transferred to the University of Oregon where he graduated with a BA in Political Science. He most recently served as Director of Technology and Innovation in the Office of Los Angeles City Controller Ron Galperin. As a forward-thinking public servant, Juan focused on cutting red-tape, making government more efficient and making a meaningful difference in the lives of Angelenos. Juan loves hiking, writing, breakfast burritos, and road trips.

Sources

Kasperkevic, Jana. “The American Dream: How Undocumented Immigrants Buy Homes in the U.S.” Marketplace, Marketplace, 11 Sept. 2017, www.marketplace.org/2017/09/08/economy/american-dream-how-undocumented-immigrants-buy-homes-us.

“Language Use.” U.S. Census Bureau, 10 Oct. 2017, www.census.gov/topics/population/language-use/about/faqs.html.

Los Angeles County Assessor. “County of Los Angeles Open Data.” County of Los Angeles Open Data.

data.lacounty.gov/Parcel-/Assessor-Parcels-Data-2006-thru-2017/9trm-uz8i/data.

LURN. “Boyle Heights Property Ownership, Displacement, and Recommendation Report: Understanding the Needs of a Neighborhood at a Crossroads.” April 2018. http://static1.squarespace.com/static/5cc9edf1af4683c0da44bd62/5ccb78317de07533f0a5c13e/5ccb783b7de07533f0a5c3e1/1556838459126/FinalReport_LURN_V2.pdf?format=original

Painter, Gary D, and Stuart A Gabriel. “Why Affordability Matters.” UCLA Anderson, www.anderson.ucla.edu/Documents/areas/ctr/ziman/AH-Policy-Brief_Gabriel-Painter_08.29.17.pdf.

Passel, Jeffrey, and D’Vera Cohn. “A Portrait of Unauthorized Immigrants in the United States.” Pew Research Center, 14 Apr. 2009, www.pewhispanic.org/2009/04/14/iv-social-and-economic-characteristics/.

“Quick Facts.” United States Census Bureau, United States Census Bureau, 1 July 2016, www.census.gov/quickfacts/fact/table/losangelescountycalifornia/PST045216.

Semple, Kirk. “Immigrants Who Speak Indigenous Languages Encounter Isolation.” The New York Times, The New York Times, 10 July 2014, www.nytimes.com/2014/07/11/nyregion/immigrants-who-speak-indigenous-mexican-languages-encounter-isolation.html.

“The Power of Place.” Boyle Heights Project: Power of Place, Japanese American National Museum, 2002, www.janm.org/exhibits/bh/exhibition/timeline.htm.

“Undocumented Immigrants’ State & Local Tax Contributions.” ITEP, Institute on Taxation and Economic

Policy, 1 Mar. 2017, itep.org/undocumented-immigrants-state-local-tax-contributions-2/.

Zillow, Inc. “Boyle Heights Los Angeles CA Home Prices & Home Values.” Zillow, 31 Dec. 2017, www.zillow.com/boyle-heights-los-angeles-ca/home-values/.

Photo Attributions

Cover Photo: Photo courtesy of Istock/peeterv

Photo 1: Photo courtesy of Istock/anouchkaJorge Villaba

Photo 2: Photo courtesy of Istock/Jorge Villaba

Photo 3: Photo courtesy of Istock/SamyStClair